Medicare Part D Formularies: How Generic Coverage Works in 2026

Jul, 12 2026

Jul, 12 2026

Prescription drug costs used to be a guessing game for millions of Americans on Medicare. You’d pick up your pills, hand over your card, and hope the price wasn’t higher than last month. That uncertainty has changed dramatically with the updates to Medicare Part D, which is the federal program that provides prescription drug coverage to Medicare beneficiaries through private insurance plans. Since its launch in 2006, Part D has served over 51 million people, but the way it handles generic drugs-the workhorses of modern medicine-has evolved significantly.

In 2026, the rules are clearer, and the savings are real. Thanks to changes from the Inflation Reduction Act, there is now a hard cap on what you pay out of pocket. But to actually save money, you need to understand how formularies, which are the specific lists of covered medications maintained by each Medicare Part D plan, work. Specifically, you need to know where generic drugs sit on those lists and how the tiered pricing structure affects your wallet.

What Is a Formulary and Why Do Tiers Matter?

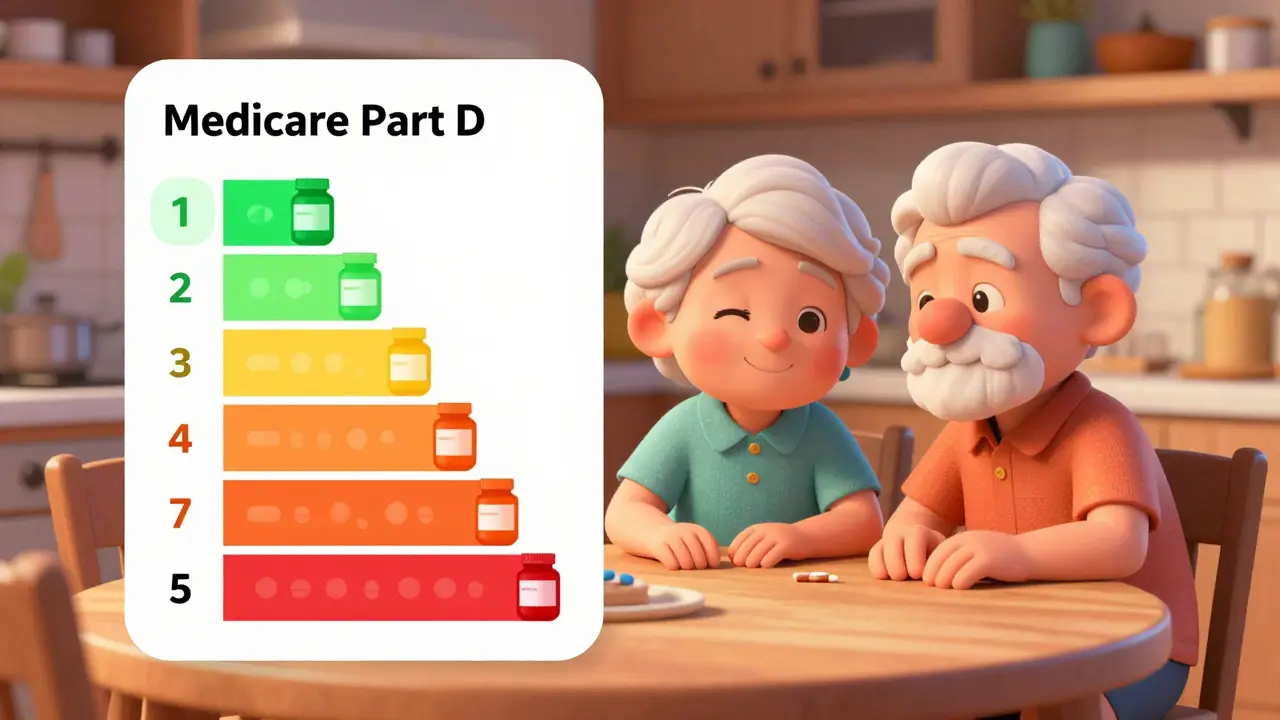

Think of a formulary as a menu. Each Medicare Part D plan creates its own menu of covered drugs. This isn't random; it’s carefully designed to balance cost and access. The key feature of this menu is the "tier" system. Tiers group drugs based on their cost to the plan and, consequently, your share of the bill.

Generic drugs almost always live in the lowest tiers. Here is how the typical 2026 structure looks:

- Tier 1 (Preferred Generics): These are the cheapest options. You usually pay a small fixed copay, often between $0 and $15 for a 30-day supply.

- Tier 2 (Non-Preferred Generics): These are still generics, but they might cost slightly more for the insurer to buy. You might pay a percentage of the cost (coinsurance) or a higher fixed fee, sometimes up to $40.

- Tier 3 (Preferred Brand-Name Drugs): Brand names that the plan has negotiated good rates for.

- Tier 4 (Non-Preferred Brand-Name Drugs): More expensive brands with higher copays.

- Tier 5 (Specialty Drugs): High-cost medications, often injected or infused, requiring special handling.

The goal is simple: if a generic version exists, the plan wants you to take it because it saves everyone money. By placing generics in Tier 1 and 2, plans incentivize you to choose them over pricier brand-name alternatives.

The 2026 Cost Structure: Deductibles and Caps

Understanding the tiers is only half the battle. You also need to know how much you pay at each stage of the year. The financial landscape shifted heavily in 2025 and continues into 2026 due to the Inflation Reduction Act. Let’s break down the phases for 2026.

| Phase | Description | Your Typical Cost for Generics |

|---|---|---|

| Deductible Phase | You pay 100% of drug costs until you hit the annual deductible. | $0 - $590 (depending on your plan's deductible) |

| Initial Coverage | After the deductible, you and the plan share costs until you hit the out-of-pocket threshold. | 25% coinsurance or fixed copay (e.g., $10-$20) |

| Catastrophic Coverage | You have spent enough out-of-pocket for the year. Costs drop significantly. | $0 for generics |

The biggest change is the out-of-pocket cap, which is a limit on the total amount a beneficiary pays for covered drugs in a calendar year. In 2026, once you spend $2,100 out of pocket (this includes deductibles, copays, and coinsurance), you enter catastrophic coverage. From that point on, you pay $0 for your generic prescriptions for the rest of the year. This eliminates the old "donut hole" anxiety where costs would spike unexpectedly.

Note that the deductible for 2026 is expected to remain around $590, though some plans offer $0 deductibles. If you take multiple generics, a $0 deductible plan can save you hundreds of dollars right at the start of the year.

How Plans Decide Which Generics to Cover

You might wonder, "Why does my plan cover Generic A but not Generic B, even though they treat the same condition?" It comes down to negotiations and committee decisions.

Every Part D plan has a Pharmacy and Therapeutics (P&T) Committee. This group consists of practicing physicians and pharmacists who review drugs based on safety, efficacy, and cost. They decide which generics go into Tier 1 versus Tier 2. Often, this depends on which manufacturer the plan has secured the best bulk price from.

However, the government sets strict guardrails. Under federal regulations (42 CFR §423.120), plans must include at least two chemically distinct drugs in every therapeutic class. For six protected classes-including antidepressants, antipsychotics, and immunosuppressants-plans must cover 100% of available generics. This ensures you aren't left without essential mental health or transplant medications just because one brand was cheaper for the insurer.

Common Pitfalls with Generic Substitution

Even with clear rules, confusion happens. One common issue is "therapeutic interchange." Sometimes, a pharmacist will substitute one generic for another equivalent one. While medically safe, this can cause billing issues if the substituted generic is on a different tier or not on your formulary at all.

For example, you might be prescribed a generic blood pressure medication. Your doctor writes for Brand X Generic. The pharmacy swaps it for Brand Y Generic because it’s in stock. If your plan only covers Brand X in Tier 1, but Brand Y is Tier 2 or excluded, you could face a surprise charge. Always check the bottle label against your plan’s formulary list. If there’s a mismatch, call your plan’s customer service immediately before paying full price.

Another pitfall is ignoring the Annual Notice of Change (ANOC). Every fall, plans send this letter detailing any changes to their formularies for the coming year. Data shows that about 37% of plans adjust at least one generic’s tier placement annually. If your favorite $10 generic moves to Tier 2, your cost could double. Reviewing this document is crucial for budgeting.

Strategies to Maximize Your Savings

So, how do you use this knowledge to keep more money in your pocket? Here are actionable steps tailored for 2026.

- Use the Plan Finder Tool Early: Don’t wait until enrollment season opens. Go to Medicare.gov’s Plan Finder tool. Enter your specific generic medications. Compare plans not just by premium, but by the estimated yearly cost for your drugs. Research suggests beneficiaries who use this tool save an average of $427 annually.

- Look for $0 Deductible Plans: If you take daily generics, find a plan with no deductible. You’ll start sharing costs immediately rather than paying full price until you hit $590.

- Request a Coverage Determination: If your necessary generic isn’t on the formulary, don’t give up. You can request a coverage determination. Historically, about 83% of these requests result in approval, especially if your doctor supports the medical necessity.

- Check for Mail-Order Options: Many plans offer lower copays for 90-day supplies sent via mail-order pharmacies. If you’re stable on your generics, switching to mail order can reduce administrative fees and per-pill costs.

- Monitor Authorized Generics: Some brand-name companies sell "authorized generics"-the exact same pill sold under a generic name. These can sometimes be confusingly placed on formularies. Verify if your plan treats them as true generics (Tier 1) or as brands (Tier 3+).

Looking Ahead: What’s Changing in Generic Coverage?

The landscape is shifting toward greater transparency and lower costs. Starting in 2026, CMS requires plans to include a "generic price comparison tool" in their member portals. This helps you instantly see if a cheaper therapeutic alternative exists for your condition.

Furthermore, the Medicare Drug Price Negotiation Program, mandated by the Inflation Reduction Act, is beginning to impact the market. While direct negotiations for specific generics start rolling out more broadly in later years, the pressure is forcing manufacturers to lower prices proactively. Analysts project that by 2027, nearly 95% of Part D beneficiaries will have access to $0 copays for at least half of commonly prescribed generics.

For now, your best defense is information. Know your tiers, watch your out-of-pocket spending relative to the $2,100 cap, and never assume a generic is covered without checking your specific plan’s formulary. Small adjustments in plan selection can lead to significant savings over time.

What is the difference between Tier 1 and Tier 2 generics?

Tier 1 generics are "preferred" by your insurance plan, meaning they have negotiated the lowest prices. You typically pay a low fixed copay (e.g., $5-$15). Tier 2 generics are non-preferred; they may cost the plan more to purchase, so you pay a higher copay or a percentage of the drug's cost (coinsurance).

Is there a cap on how much I pay for generic drugs in 2026?

Yes. Due to the Inflation Reduction Act, there is a hard out-of-pocket cap of $2,100 in 2026. Once your total spending (deductibles, copays, and coinsurance) reaches this amount, you enter catastrophic coverage and pay $0 for generics for the rest of the year.

Can my plan refuse to cover a generic drug?

Generally, no. Federal rules require plans to cover most commercially available generics, especially in protected classes like antidepressants and immunosuppressants. However, they can exclude certain drugs if they meet specific regulatory criteria, such as being used primarily for cosmetic purposes. If your drug is excluded, you can appeal via a coverage determination.

Why did my generic drug move to a higher tier?

Plans update their formularies annually based on new contracts with manufacturers. If a plan secures a better deal for a different generic in the same class, they may move your current drug to a higher tier to encourage switching. Check your Annual Notice of Change (ANOC) each fall for these updates.

Do I have to pay the deductible for generic drugs?

It depends on your plan. Most plans have a deductible (around $590 in 2026) that you must pay before coverage kicks in. However, many plans offer $0 deductibles specifically for Tier 1 preferred generics. Look for these plans if you want to avoid upfront costs.